On October 4, 2024, the Centers for Medicare and Medicaid Services (CMS) released a proposed rule titled “HHS Notice of Benefit and Payment Parameters for 2026” (link) with an accompanying fact sheet (link). CMS is accepting comments until November 12, 2024.

The annual ADVI Instant: CMS Releases 2026 Notice of Benefit and Payment Parameters (NBPP) issues standards for insurance companies and the state and federal Marketplaces. This year’s proposed rule addresses policies related to PrEP and Hepatitis C drugs, beneficiary cost sharing, enrollment and quality reporting, and requirements for standardized and non-standardized plans.

Notably, CMS is proposing to create a new type of risk adjustment factor called Affiliated Cost Factors (ACF) to account for expenses or services not directly affiliated with a diagnosis or condition, e.g., preventive drugs such as human immunodeficiency virus (HIV) pre-exposure prophylaxis (PrEP). CMS is seeking feedback on the creation of ACFs, the suitability of PrEP as an ACF, and other expenses or services that should be considered as a potential new ACF.

Additionally, HHS specified that future rulemaking is forthcoming related to the use of copay accumulators and maximizers. HHS and the Departments of Labor and Treasury “intend to issue a future notice of proposed rulemaking address the issues arising out of HIV and Hepatitis Policy Institute et al. v. U.S. Department of Health and Human Services et al., Civil Action No. 22- 2604 (D.D.C. Sept. 29, 2023), namely, the applicability of drug manufacturer support to the annual limitation on cost sharing.” Below, ADVI provides an overview of select, relevant highlights from this rule. If you have any questions or would like further information, please do not hesitate to contact your ADVI Account Manager.

Proposed Inclusion of Pre-Exposure Prophylaxis (PrEP) in the HHS Risk Adjustment Adult and Child Models as an Affiliated Cost Factor (ACF)

CMS is proposing to include human immunodeficiency virus (HIV) pre-exposure prophylaxis (PrEP) as a new type of factor called an Affiliated Cost Factor (ACF) in risk adjustment models for 2026. Currently, risk adjustment factors only apply to active conditions and PrEP is modeled as a preventive service with zero cost sharing.

CMS analysis of PrEP usage found statistically significant, substantial differences in PrEP prevalence between insurers, suggesting that PrEP services pose a risk of adverse selection.

CMS considered other options (e.g., incorporating PrEP as a prescription drug category (RXC) or hierarchical condition category (HCC)), but the lack of diagnosis/condition rendered them inappropriate, so it proposes the creation of the new ACF that would not indicate an active medical condition.

Because of cost disparities between generic PrEP and long-acting injectable forms, CMS is considering excluding generic PrEP from the PrEP ACF, if adopted.

CMS is proposing a set of principles to guide these new factor determinations. The principles state that ACFs should:

Be clinically meaningful and comprised of NDCs that do not indicate a diagnosis or condition,

Meaningfully predict total medical and drug expenditures

Have adequate sample size to allow accurate/stable expenditure estimates

Be treated hierarchically (i.e., the presence of relevant HCC or RXC should preclude the application of ACF)

Not carry a negative payment weight and should carry an equal or lesser weight than the HCC or RXC factors that reflect the disease (in the example of PrEP, HIV/AIDS factors)

Assign NDCs or service codes to only one ACR or RXC variable

Have low risk of inappropriate prescribing

CMS believes PrEP meets some of the above listed principles but identified challenges with others. As such, it is considering modifying the Anti-HIV agent RXC 1 or placing the PrEP ACF in a hierarchy with RXC 1 but define no restrictions between PrEP and HCC 1 (HIV/AIDS).

CMS is soliciting comments on creating a new ACF category of factors to account for expenses and services that don’t meet HCC or RXC criteria, defining an ACF for PrEP, feedback on PrEP alignment with ACF principles, and whether any similar medical expenses or services (aside from PrEP) should be considered for potential new ACFs.

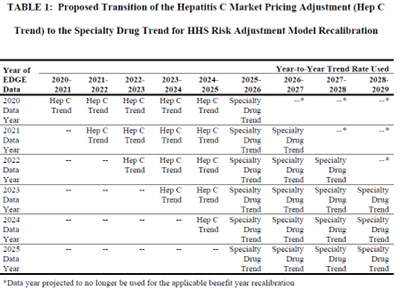

Pricing Adjustment for the Hepatitis C Drugs

Since 2020, the HHS risk adjustment models have adjusted plan liability to account for Hepatitis C drugs. In reassessing the need for this adjustment, CMS has determined that it is appropriate to begin phasing out the Hepatitis C drug adjustment and start trending the cost of these drugs consistent with others in the models. CMS believes this approach will align with its expectation for Hepatitis C drug cost growth to be similar to specialty drug growth in the future.

As CMS will trend enrollee data from 2020 – 2022 to project costs in 2026, it is proposing to continue to trend Hepatitis C drugs separately through 2025, and then apply a specialty drug trend factor rather than the Hepatitis C trend factor for 2026.

CMS would annually phase-in additional years of specialty drug trend until it is fully applied consistent with other specialty drugs in the HHS risk adjustment model. The phase-in is visually presented in Table 1 on page 50 of the proposed rule, below:

Beneficiary Cost Sharing

CMS is not proposing to change the methodology for calculating the premium adjustment percentage, the required contribution percentage, and maximum annual limitations on cost sharing and reduced maximum annual limitation on cost sharing for the 2026 benefit year.

CMS intends to publish these parameters in guidance no later than December 31, 2024.

CMS proposes to codify policies to allow insurers additional flexibility to not:

Place an enrollee in a grace period for failure to pay the full premium amount

Terminate plan enrollment after a grace period ends without outstanding premiums being paid in full

CMS notes that these proposals are meant to reduce the number of coverage terminations for enrollees who only owe a small amount of premium.

Enrollment and Quality Reporting

CMS is proposing to:

Publicly report metrics that State Exchanges and State Based Exchanges on the Federal platform (SBE-FPs) must report to CMS, including data on outreach, eligibility and enrollment policies and processes

Codify guidance requiring state exchanges to, within 60 days of receiving a report of data inaccuracy from an insurer participating in the exchange, review and resolve the insurer’s enrollment data inaccuracies and submit a report to HHS

Starting January 1, 2026, share aggregated, summary-level Quality Improvement Strategy (QIS) information publicly on an annual basis (QISs must be implemented by insurers to be certified as Qualified Health Plans (QHPs))

Information that will be publicly reported includes:

Value-based payment models used in QHPs offered by the insurer

Market-based incentives

Clinical areas addressed

Activities and measures

Note: Reported information will be limited to insurers operating in Federally Facilitated Exchanges.

Requirements for Standardized and Non-Standardized Plans

Standardized Plan Options

CMS is proposing to require issuers of standardized plans within the same product network type, metal level, or service area to meaningfully differentiate their benefit offerings, provider networks, and formularies by plan.

The “meaningful difference” standard was a previous requirement that was discontinued in the 2019 payment notice due to the decreased number of plan offerings on the Exchanges. However, CMS notes that several issues in recent years have offered indistinguishable standardized plan options, likely due to the limits on non-standardized plan options (detailed below).

Therefore, for 2026 CMS is seeking to bring back the meaningful difference standard to reduce consumer confusion and prevent unnecessary plan proliferation.

CMS notes that should its proposed policy not be sufficient in preventing “nearly identical” plans, it will consider a future version of meaningful difference that would require greater variation among plans.

Non-Standardized Plan Option Limits

CMS is proposing conforming amendments about non-standardized plan option limits to reflect that for plan year 2025 and beyond:

Issuers are limited to offering two non-standardized plan options per product network (i.e., plans that vary in terms of adult dental, pediatric dental, or adult vision coverage)

Issuers may offer additional non-standardized plan options, only if the cost sharing for chronic and high-cost conditions is at least 25 percent lower (including for prescription drugs that treat such conditions) than the two non-standardized plan options per product network

Impact of Advanced Premium Tax Credits (APTCs) Extension

Generally, CMS notes that if Congress passes an extension of the Advanced Premium Tax Credits (APTCs) this would significantly alter CMS’ estimates around costs, enrollment projections, or the finalization of proposed risk adjustment policies between the proposed and final rule.

ADVI will continue monitoring developments and the next steps. This is a delayed release. ADVI Instant content is distributed in real-time for retainer clients. Get in touch to learn more about how we can support your commercialization, market access, and policy needs.